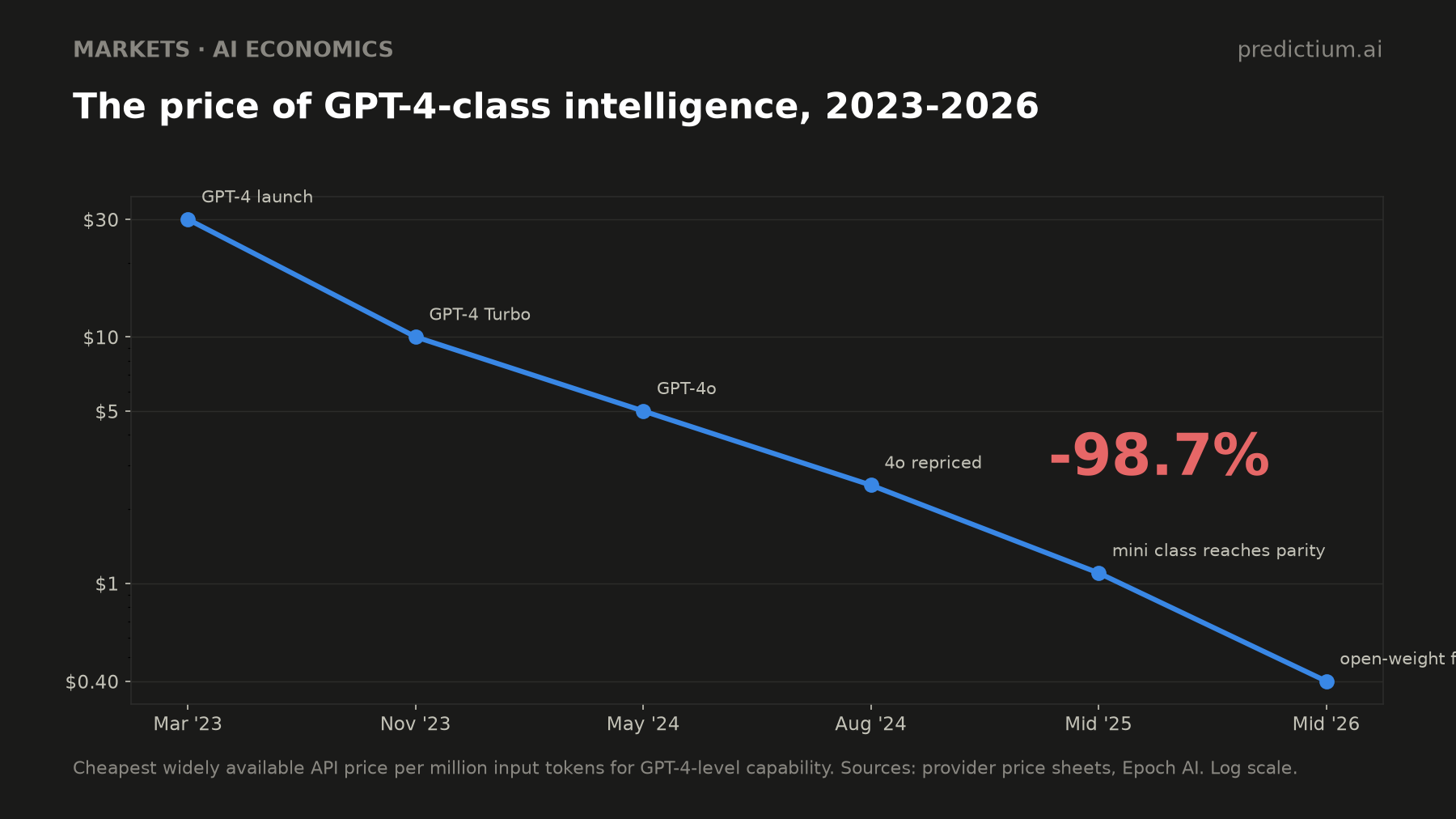

In March 2023, OpenAI charged $30 per million input tokens for GPT-4. Today you can buy that same level of capability for about 40 cents. That is a 98.7% price decline in roughly three years, and it happened while demand for the product grew faster than demand for almost anything in the history of software.

Nobody disputes this chart. The interesting argument is about what it means. The bulls read it as a semiconductor story: prices fall, usage explodes, revenue grows anyway, everyone wins. The bears read it as a commodity story: when your product gets 40x cheaper every year and your competitor gives away a version that is six months behind yours for free, you do not have pricing power. You have a countdown.

I want to work through what happens if the bears are right, because the market is currently priced as if they can't be.

The six-month shadow

The mechanism that worries me is not that frontier models get cheaper. It is that the gap between the best closed model and the best free one keeps shrinking, in time and in quality.

The best open-weight models today score within about 9 points of the proprietary leaders on composite benchmarks. On coding, the gap has nearly closed: open models are hitting 69 to 72% on SWE-bench Verified, which is the neighborhood the closed frontier lived in quite recently. On math and question answering, DeepSeek's latest sits at near parity with the top closed models.

Every frontier release now operates in a shadow. Six months after you ship a capability, something close enough to it exists with no meter attached. Your pricing power lives entirely inside that six-month window, and the window is what pays for everything else.

So the question that matters for the labs is brutal and specific: what fraction of paying workloads actually needs this month's frontier rather than last year's, which is now nearly free? Nobody publishes that number. But every price cut suggests the labs' own answer is "less than we'd like."

The bill is already enormous

Here is what the sell side of this trade looks like in 2026.

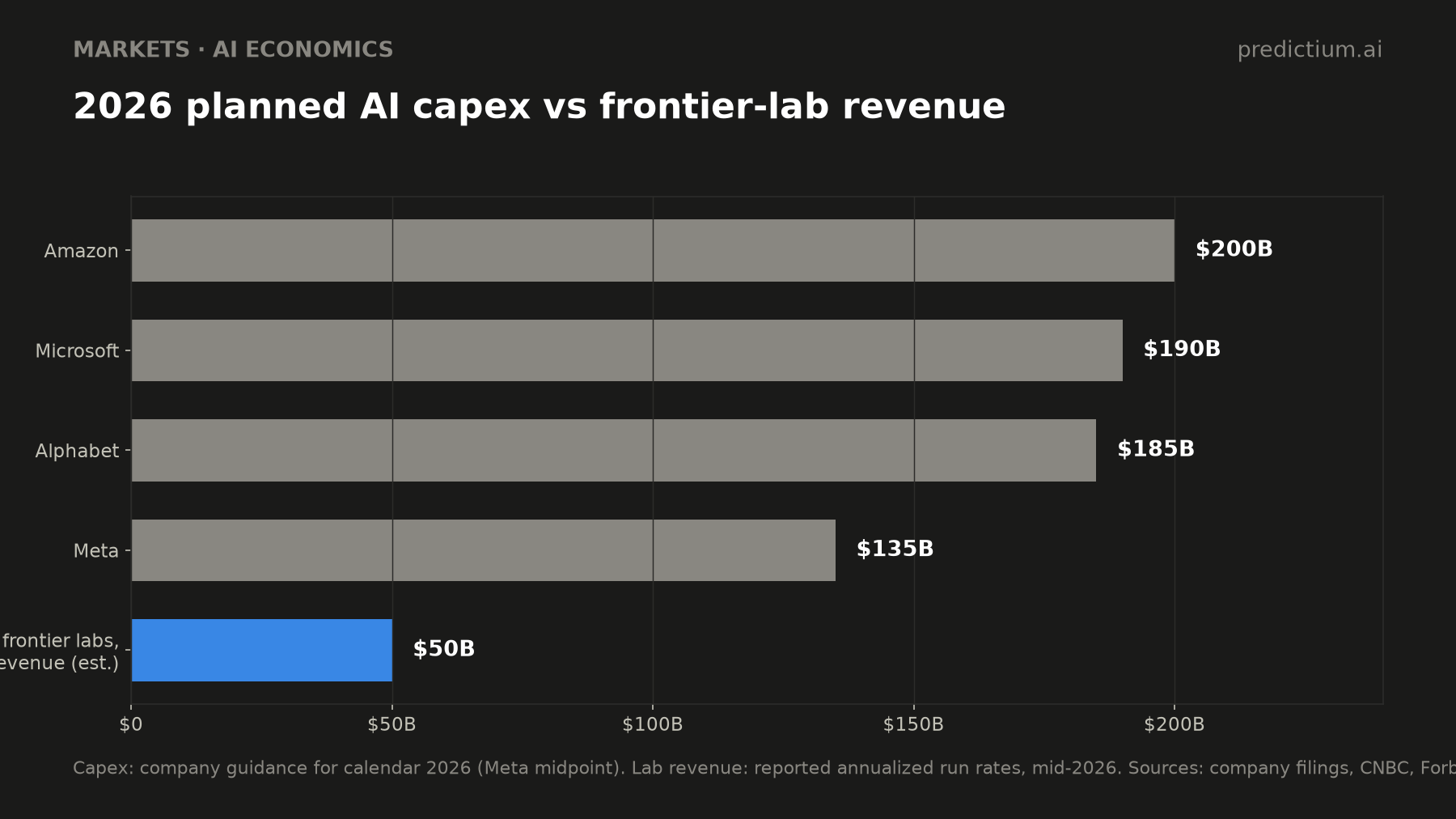

The four biggest hyperscalers plan to spend somewhere around $700 billion on AI infrastructure this calendar year. Amazon alone guided to $200 billion, which is more than double what it spent last year. Against that: the combined revenue run rate of all the frontier labs is somewhere around $50 billion, and the two biggest are still burning cash. OpenAI is reported to be losing on the order of $14 billion this year on roughly $20 billion of revenue.

Meanwhile the private market has priced OpenAI at a reported $852 billion and Anthropic at $965 billion. Those are luxury-brand multiples on businesses whose core product has been repricing downward at 40 to 90% per year, funded by infrastructure spending that is 14 times the revenue of the entire model layer.

The standard defense is that this is AWS in 2006: spend ahead of demand, look insane, collect a monopoly later. Maybe. But AWS sold a product with enormous switching costs and no free substitute. A model API has neither. Swapping one model for another is, increasingly, a config change. That is what commoditization means.

Who keeps the margin

If intelligence itself trends toward the price of electricity, the value doesn't vanish. It moves. Three places it can go:

The compute layer. Nvidia and the hyperscalers sell shovels, and shovels held margin in every gold rush. But shovels priced for permanent scarcity are exposed to the same efficiency curve that crushed token prices. The chart above is, in part, a bet by four companies that the efficiency gains stop before their depreciation schedules catch up.

Distribution. ChatGPT has something like a billion users and a brand that means "AI" to normal people. If the underlying models are interchangeable, the consumer relationship is the asset, the way Google's homepage was the asset long after search algorithms stopped being magic. This is, quietly, the strongest bull case for OpenAI, and it has nothing to do with model quality.

The application layer. If your product uses intelligence but is not intelligence, commoditization is a gift. Your input cost fell 98% and your price didn't. This describes us, for what it's worth: Predictium's models cost less to run every quarter, and a subscription costs the same.

What does not obviously keep margin is the thing in the middle: training frontier models as a standalone business, sold by the token, at luxury valuations.

What the traders say

We run a site whose whole premise is that you should check your beliefs against a market that costs money to be wrong in. So let's do that.

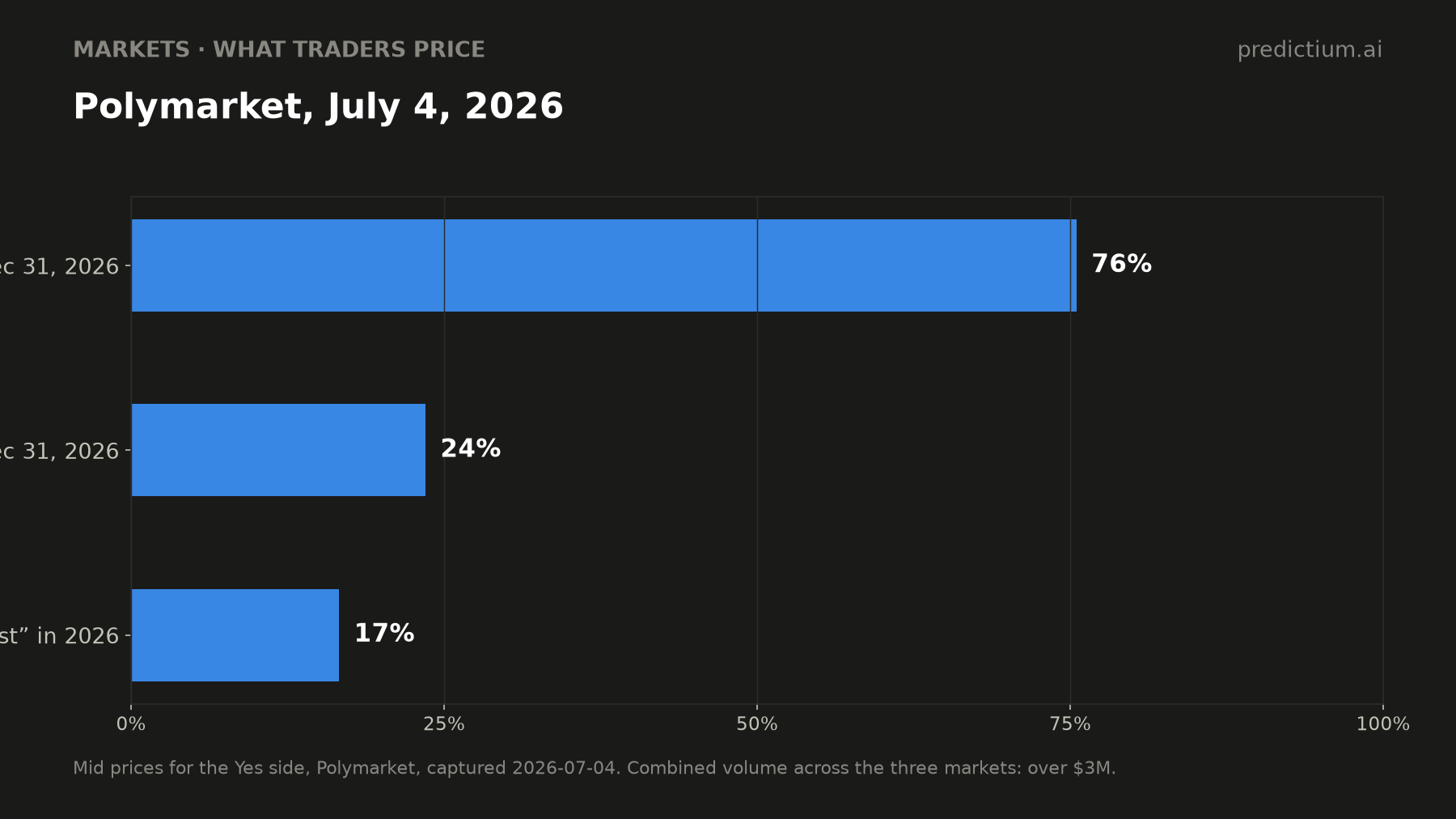

As of today, Polymarket prices an "AI bubble burst" in 2026 at about 17%. It prices an Anthropic IPO by year-end at 75%, and an OpenAI IPO by year-end at only 24%. Read together, traders with real money are saying: no crash this year, and the labs will hand the valuation question to the public markets, with Anthropic going first.

That 17% is worth sitting with. It is not nothing. As a rough comparison, our NBA model treats a 17% underdog as a live outcome, the kind that hits every few nights. Traders are assigning roughly that odds to the scenario where this all goes badly within six months, while private markets price the labs as if the odds were close to zero. One of those two prices is wrong.

An IPO, when it comes, is the moment the pricing-pressure question stops being theoretical. Public markets will demand the number private investors have not: gross margin on inference, net of the discounts, and how it trends as open weights close the gap. The margin trajectory reported this year (one lab's inference margin reportedly went from 38% to over 70%) is the bulls' best exhibit. Whether it survives contact with a free substitute two quarters behind is the entire question.

What would prove me wrong

I'm on record now, so here is the falsification list, and we will keep score on it in public like we do with everything else on this site:

- Frontier prices stabilize. If the price of top-tier intelligence holds flat for four consecutive quarters while open weights keep improving, the labs have found real pricing power and the commodity thesis is wrong.

- The gap widens. If the open-to-closed benchmark gap grows again, the six-month shadow was a phase, not a trend.

- An IPO prices clean. If OpenAI or Anthropic goes public, discloses inference margins, and the stock holds its private-round valuation for a year, the market disagreed with me at the point of maximum information.

The other side of the ledger: if a frontier lab cuts prices on its flagship within a quarter of an open-weight release, or an IPO slips again while the capex keeps climbing, the squeeze is on.

We'll track all of it on Bubble Watch, next to the market prices, where being wrong costs something.